A Tale of Four Investments: How Major Real-state Asset Class Prices are on Completely Different Paths in Today's Unusual Environment

- Ian Ippolito

- Sep 8, 2025

- 6 min read

Unprecedented events have caused prices on the four primary real-estate classes to do something very unusual… completely diverge. We look at which ones are blossoming, which are coping and which are bleeding.

(Usual disclaimer: I'm just an investor expressing my personal opinion and am not an attorney, accountant nor your financial advisor. Consult your own financial professionals before making any financial decisions. Code of Ethics: To remove conflicts of interest that are rife in other clubs/sites, I/we do not accept ANY money from outside sponsors or platforms for ANYTHING. This includes but is not limited to: no money for postings, nor reviews, nor tutorials, nor gudies, nor advertising nor affiliate leads etc. Nor do I/we negotiate special terms for ourselves in the club above what we negotiate for the benefit of members. Info may contains errors so use at your own risk. See Code of Ethics for more info.)

This is an update to my previous article (from last quarter) called ”How are Alternative Asset Classes Responding in Today's Volatile Environment (and where are the Potential Opportunities and Dangers)?”

That original article discussed how tariffs, interest rates and other factors would probably influence different alternative asset classes in the short to medium term.

This new article looks at what’s actually happened since then. And we’ll focus on the 4 major real estate asset classes: Multifamily, retail, industrial and office.

Multi-family: Riding the tariff wave

As discussed previously, many analysts expected multi-family prices to be the big winner from tariffs. That’s because tariffs increase the cost of construction materials (such as prices for steel, lumber and copper) and inflation causes construction labor costs to increase. And when this happens, new construction projects are forced to halt.

And this matters to all real-estate. But it’s especially important to multi-family because it’s been suffering from a glut of post-pandemic supply. And this caused a pricing downturn (starting in 2022). So, if tarrifs kill new supply, then multi-family prices should rise over the next year and half.

So what’s happened so far?

According to a recent Wall Street Journal article,

Apartment absorption, a metric of rental demand that measures the change in how many units are leased, was higher last quarter than any other fourth quarter since at least 1985, according to real-estate firm CBRE.

In a recent BisNow article, it said that:

CBRE projects that construction starts at the middle of this year will be 74% below 2021 levels and 30% below the pre-pandemic average.

What result has this had on prices?

Here’s the latest data from the Co-star Commercial Repeat Sales Index (CCRSI) June 2025 report:

Multifamily prices are continuing to rise from the lows hit in 2023. And this is pretty much exactly what many predicted: Prices increasing over the several years.And as discussed in the last article: many tariff effects are expected to cause a delayed hit. If so, the wiping-out of new supply could occur even more rapidly in the future (and further boosting returns).

Also, larged, outsized price-gains often historically come from investing in early vintage years in a new up-cycle (and holding). So if this is indeed the start of a new one, then investors who deployed in 2024 and 2025 (and hold) could look back and find they've invested in particularly opportune vintage years.

Retail Keeps on Trucking

What about retail?

Retail was the first to recover in 2022 and since then has been slowly but steadily increasing. So how's it done more recently?

According to recent CBRE article,

“Retail development remains near all-time lows, with only 4.5 million sq. ft. delivered in Q1—well below historic norms. Elevated construction costs, labor shortages and tighter lending standards continued to constrain new projects and intensify competition among well-located assets.”

And what result has this had on prices? The CCRSI June 2025 says:

So that's good to see.

Industrial: Rough waters ahead?

How about industrial? Like retail, it recovered fairly quickly in 2022. And after remaining steady it then started slowly increasing starting in (2023). So things were looking up.

However, some predicted that tariffs could throw a monkey wrench into things.

So what’s happened more recently? The CCRSI June 2025 data says:

That’s a troubling sign. Not only has the brief recovery stopped, but things are moving in the wrong direction. What’s going on?

According to the Wall Street Journal,

“Companies paused leasing due to tariff uncertainty, opting to use existing space for inventory”. And as as result, warehouse vacancies have soared to the highest level in more than 11 years (to 7.1%)"

Additionally, Yardi Matrix reports that,

“Tariff policy led to fewer ships in Western ports in May, while firms and logistics providers look for ways to mitigate cost increases....Uncertainty around tariffs has delayed leasing decisions for many occupiers, slowing the rate at which recently delivered new supply is being absorbed. Uncertainty has also led to fewer interest rate cuts than previously anticipated, keeping costs for construction loans elevated and putting downward pressure on starts.

Perhaps the biggest threat to a rebound in industrial starts, however, is a 50% tariff on imported steel. U.S. firms imported $32 billion in steel in 2024, and current demand far exceeds current production capacity. Further complicating matters, the U.S. and Canadian steel industry supply chains are integrated across the border”

So, industrial could be in for a rough time.

Also, as of this week, additional tariffs have at least been threatened. And no-one knows if:

Perhaps they will be enacted (after no deal is struck)

Perhaps deals will be struck to avoid them.

Perhaps the U.S. will back down on one or more demands (i.e. if U.S. markets crash and compelling the so-called TACO trade to prevail).

Or some combination of the above happens.

Whatever happens…industrial investors will want to monitor current events closely.

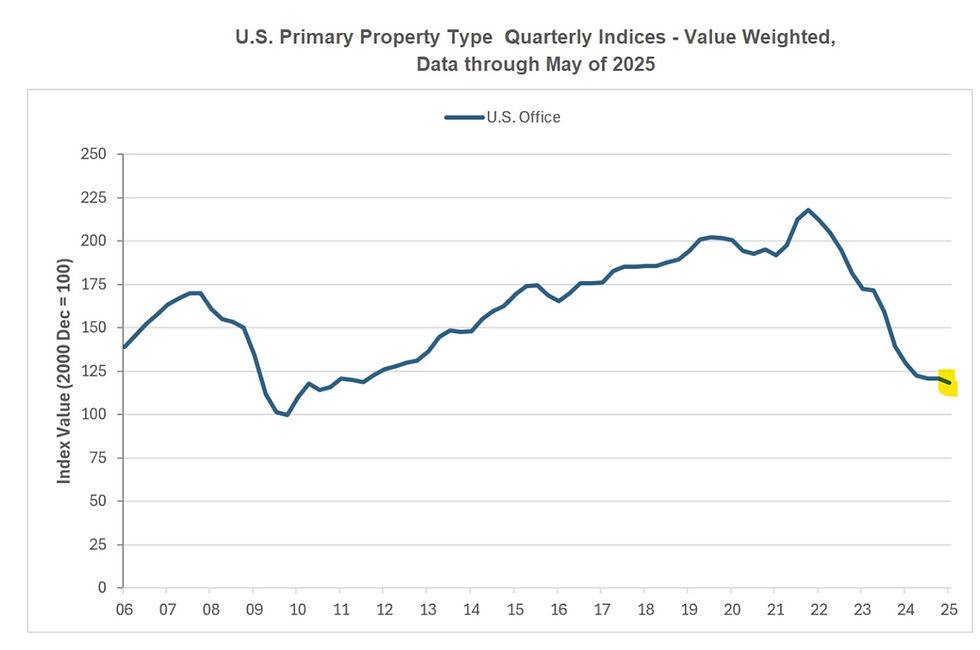

Office's Bleeding Won’t Stop

Poor office investors. It's hard not to feel bad when you look at where they are now.

In the modern financial era (i.e. post World War II), a simple “buy and hold” strategy has worked incredibly well in virtually every real-estate asset class.

And despite the recent downturn, all the other real estate asset class are up substantially from their previous lows (back in 2009 after the Great Recession).

The one glaring exception is office:

It’s barely moved up from the 2009 lows. And anyone who has bought since then is probably looking at losses.

What’s happening here? The problem is that office is undergoing a fundamental sea-change. After Covid 19, many workers are no longer willing to return to the pre-pandemic standard of mandatory office hours.

And so office has performed the worst of all the major real estate asset classes. From 2022 through 2024, it’s tumbled a painful 38%. And finally in 2024, it mercifully stabilized.

So many office investors hoped that the worst was finally over and a recovery would soon be on the way.

Is that happening? Here’s the latest CCRSI data from the June 2025 report:

Ouch. So prices are not just failing to recover but they are now dropping (yet again). What’s the deal with this?

According to Moody’s,

“The office vacancy rate was at 20.7% in Q2 2025, up from 20.4% in Q1 2025, and up from 20.1% in Q2 2024. This is the highest vacancy rate on record and is above the 19.3% peak during the S&L crisis.”

That is unfortunately moving in the wrong direction.

And according to Business Journal data:

“11 office markets tracked by Moody's posted negative net absorption in Q2, and four of those — Seattle, Boston, Chicago and suburban Virginia — had negative net absorption in excess of 500,000 square feet

So many people had really hoped that office’s bleeding had stopped. But, unfortunately, it looks like the patient has not yet stabilized.

And, office investors will want to monitor emerging events very closely.

Digging deeper / Learning More

This interesting topic (and much more) is being discussed with thousands of investors in the Private Investor Club.

If you're already a member, click here to discuss further:

If you're not yet a member, then joining is free.

To protect all members and keep the conversations useful and confidential, all applicants are required to verify that they're solely investors (and not investment sponsors, platforms or their affiliates)

Click here to learn more or to join.